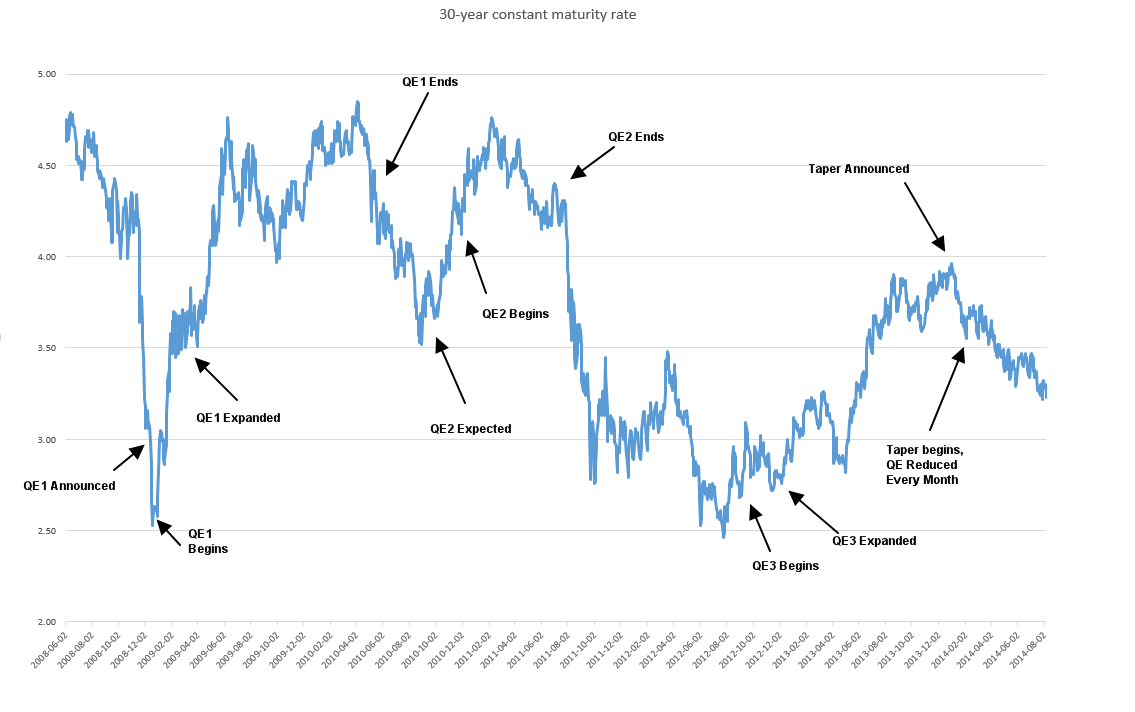

30 Year Treasury Bond Yield and QE

This chart shows that interest rates rise during QE and fall after.

×

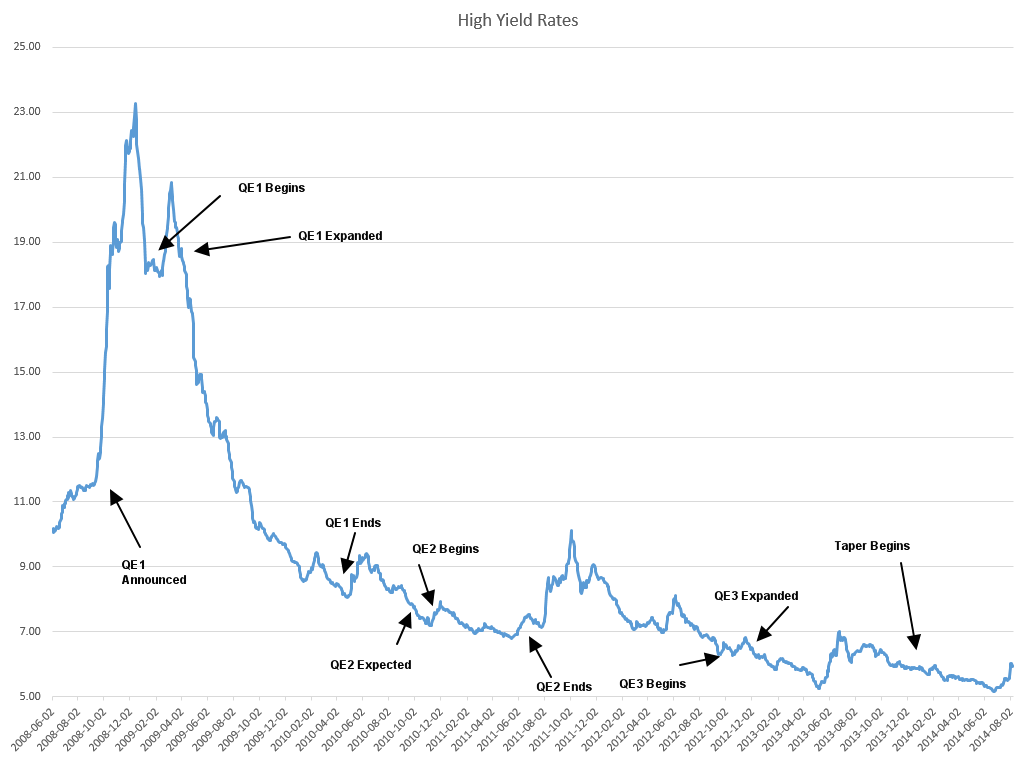

Junk Bonds and QE

It appears that junk bonds have benefitted quite a bit from QE, however this could also just be coincidental. This chart uses the BofA Merrill Lynch US High Yield Master II Effective Yield© to visualize junk bond yields. Data from FRED.

×

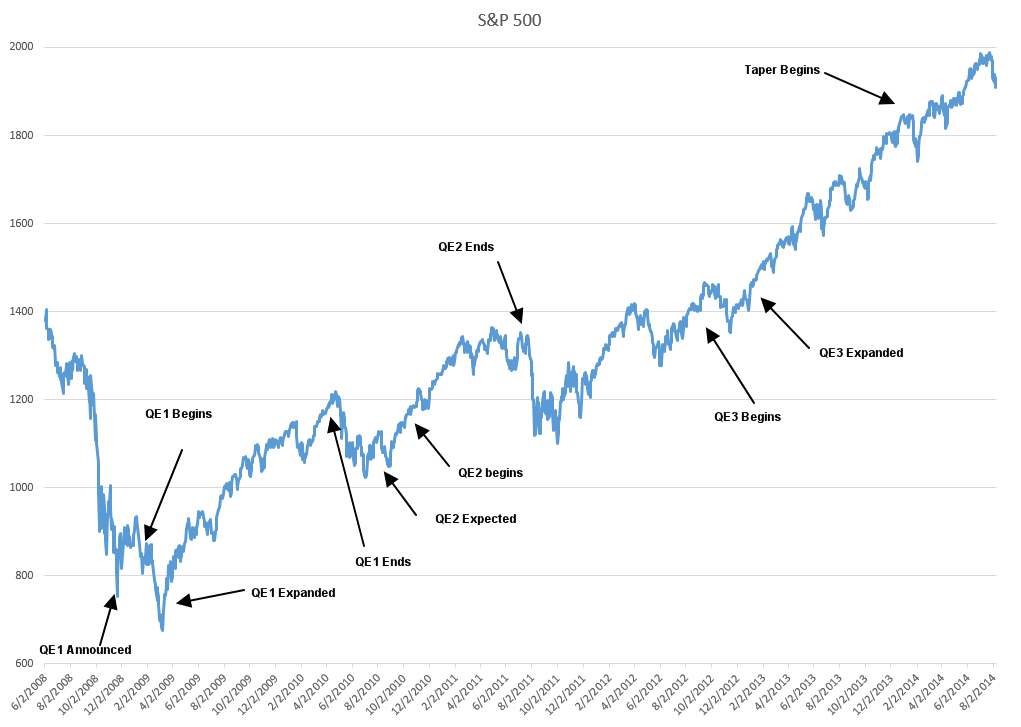

Stocks and QE

This chart shows the S&P 500 and QE. Stocks seem to benefit from QE.

×

The Not So Inevitable Rise in Interest Rates

Sunday 08/10/14

This week I want to touch on a subject that seems to be confusing the so-called experts. One of the most common themes I keep hearing is that a rise in interest rates is inevitable. The reasoning for this assumption is that as the Fed winds down its policy of quantitative easing, interest rates will rise. On the surface this seems to make sense, because if the Fed is buying less treasuries and mortgage backed securities the artificial demand for these securities will fall. As any introductory economic class will tell you, when demand falls so does price. When bond prices fall interest rates rise, therefore now that the Fed is ending its policy of quantitative easing, we should see a rise in interest rates, right?

Wrong

There was a near unanimous consensus that interest rates were going to rise at the beginning of 2014 and the only question was by how much. However, the exact opposite has happened and many analysts seem perplexed as to why. After all, the Fed has been tapering by $10 Billion every month all year. The problem is that when you look at the data it seems to suggest that quantitative easing raises interest rates. While this may seem counterintuitive, I put together this chart on the right that shows interest rates on 30 year treasury bonds and marked where QE has occurred. When you strip out all market noise and just look at the big picture it is hard to claim that quantitative easing lowers interest rates.

Quantitative easing doesn’t affect interest rates the same way that the federal funds rate target does, which was lowered to 0-0.25 at the end of 2008 where it has remained ever since. Much of the impacts of quantitative easing were unknown and still are, but the evidence seems to suggest that in its current form, it benefits corporate borrowers, especially lower grade corporate borrowers. The next chart shows below investment grade corporate bond yields (Also known as junk bonds or high yield bonds) over the same time period. As recently as June, junk bond yields reached record low rates, but by mid-July investors began pulling money out of junk bond funds and the most recent data showed that investors pulled a record $7.1 Billion out of junk bond funds. This should be alarming as the amount is even greater than during the 2008 crisis. Junk bond prices tend to behave more like stocks than bonds, because they involve more risk. I also included a chart of stock prices and quantitative easing.

So why does quantitative easing lower rates on junk bonds, but not treasuries. When the fed purchases long term treasuries from the banks, they are just exchanging the bank’s long term treasury bonds with reserves held at the fed. The interest rate on those reserves will be significantly lower than the rate that they were earning (Interest on reserves held with the fed is 0.25%). Needless to say, bank shareholders are not going to be happy with 0.25% so the banks will move out on the risk curve and will instead find a home for that money in higher yielding assets, such as stocks and corporate bonds. Therefore, as quantitative easing winds down, unless economic growth and inflation rise, stocks and high yield bonds could suffer.

| Index | Closing Price | Last Week | YTD |

|---|---|---|---|

| SPY (S&P 500 ETF) | 193.24 | 0.19% | 4.63% |

| IWM (Russell 2000 ETF) | 112.27 | 1.0% | -2.68% |

| QQQ (Nasdaq 100 ETF) | 94.9 | 0.0% | 7.89% |

30 Year Treasury Bond Yield and QE

Junk Bonds and QE

Stocks and QE