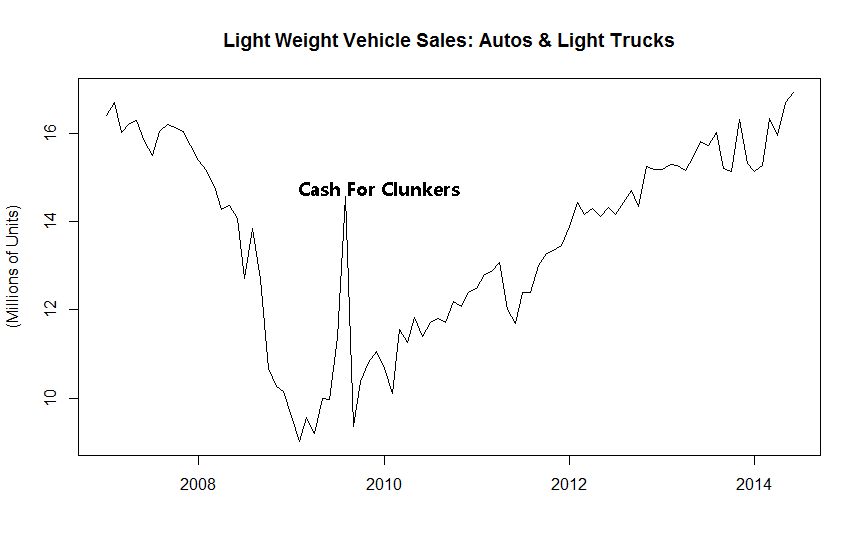

Auto sales recovery

This chart shows the recovery from the recession in 2009. The large spike is from the cash for clunkers program.

×

Everyone's Approved

Signs like this are common at used car dealers. This particular advertisement is from a Canadian company.

×

Subprime Auto

Monday 07/21/14

Last week Janet Yellen met with the house and senate banking committees to provide her biannual report on the economy and monetary policy. While most of what she reported was consistent with previous Fed minutes, she was much more hawkish regarding specific equity valuations. This was the line that caught the market’s attention:Nevertheless, valuation metrics in some sectors do appear substantially stretched—particularly those for smaller firms in the social media and biotechnology industries, despite a notable downturn in equity prices for such firms early in the year. Moreover, implied volatility for the overall S&P 500 index, as calculated from option prices, has declined in recent months to low levels last recorded in the mid-1990s and mid-2000s, reflecting improved market sentiment and, perhaps, the influence of “reach for yield” behavior by some investors.

I have already written about my concerns regarding equity valuations in certain sectors here and here. While I agree with Yellen that certain valuations are substantially stretched, I think the stretched companies are more difficult to define and can’t be broadly applied to entire sectors. This week I want to look at one particular industry that is booming from insatiable “reach for yield” as well as the associated risks.

Subprime Auto Lending

One bright spot in the slow growth recovery has been automobile sales. The chart on the right shows the recovery. What is concerning about the rise in automobile sales is that it has not been accompanied by a rise in incomes, which means that it is driven by debt. Much of this growth has come from a resurgence in subprime lending (subprime refers to borrowers with credit scores below 640). Subprime lending generally carries a much higher interest rate, which can be attractive to income investors who are seeking a higher return than traditional bonds. However, subprime lending is also accompanied by much higher default rates particularly in times of economic stress.

Before going into more detail on the mechanics of this new subprime auto lending boom, let’s take a quick look back on the subprime mortgage bubble. Home loans were pushed on borrowers who had poor credit scores and low incomes by a host of new lenders with unscrupulous practices. In many cases the applications included stated income only and were often made up on the spot by the lender, just to ensure that the borrower would qualify. This recent article from the New York Times describes some of the strong-arm tactics used by many lenders as well as income falsification. In much the same way, new subprime auto lenders have been popping up in recent years often funded by private equity companies. Of course, these lenders would not be able to extend a significant amount of financing if they were directly lending money to these consumers.

Subprime lenders are transferring the risk to investors who are reaching for yield. This press release describes a recent $320 million asset backed securitization (ABS) that was raised from $275 million due to significant investor demand. Just like the subprime mortgage backed securities, these are packaged by Wall Street and sold to pensions, mutual funds, and other institutional investors who are seeking a higher yield. In some cases, the loans have not even been made yet, but instead investors are blindly relying on the lenders to make future loans, this process is described in more detail here.

Institutional investors receive payments from subprime borrowers in exchange for taking on the credit risk, subprime lenders and Wall Street realize their gains upon the sale of the ABS. These securities contain different classes that have a range of credit ratings, for example the aforementioned ABS has 5 different classes ranging from A1+ to BBB. The different classes or tranches created a serious problem in the subprime housing crisis, because the senior tranches were paid in full in the event a certain predetermined number of defaults, but if the lender were to modify the loans to reduce the principal owed, that would negatively affect the senior holders. While this will probably not lead to contagion in falling car prices in the same way that it did for housing, it will likely mean more defaults and implies extremely high risk in the lower classes.

Investor demand for these loans is extremely high and does not show any signs of abating despite concerns from the fed. As long as interest rates remain low, institutional demand will remain high because of fiduciaries who need to achieve a certain return that simply cannot be achieved through traditional investments. This also highlights how none of the core problems involved in the previous subprime crisis have been resolved.

| Index | Closing Price | Last Week | YTD |

|---|---|---|---|

| SPY (S&P 500 ETF) | 197.7099 | 0.05% | 6.85% |

| IWM (Russell 2000 ETF) | 114.23 | -1.88% | -1.38% |

| QQQ (Nasdaq 100 ETF) | 96.12 | 0.44% | 9.14% |

Auto sales recovery

Everyone's Approved