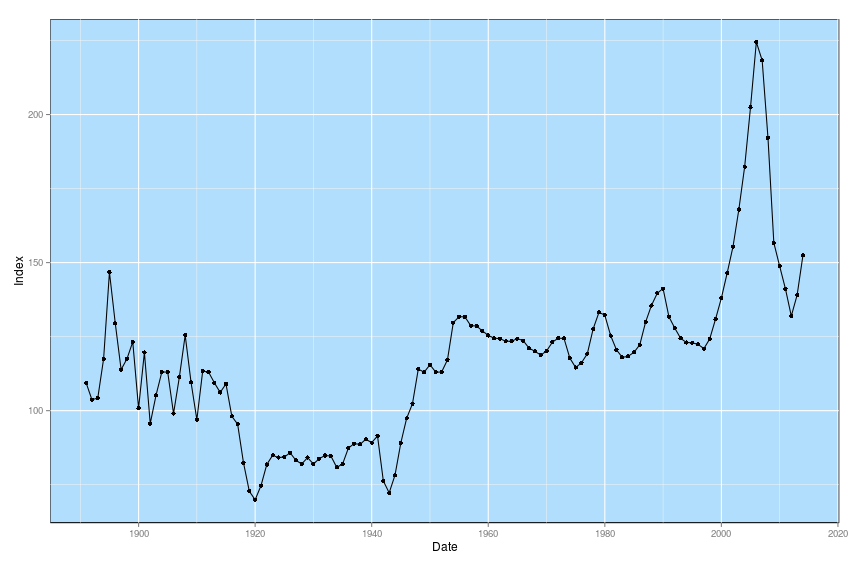

Case Shiller Home Price Index

This chart shows home prices adjusted for Inflation over the long term. As you can see there is no clear long term trend in aggregate home prices.

×

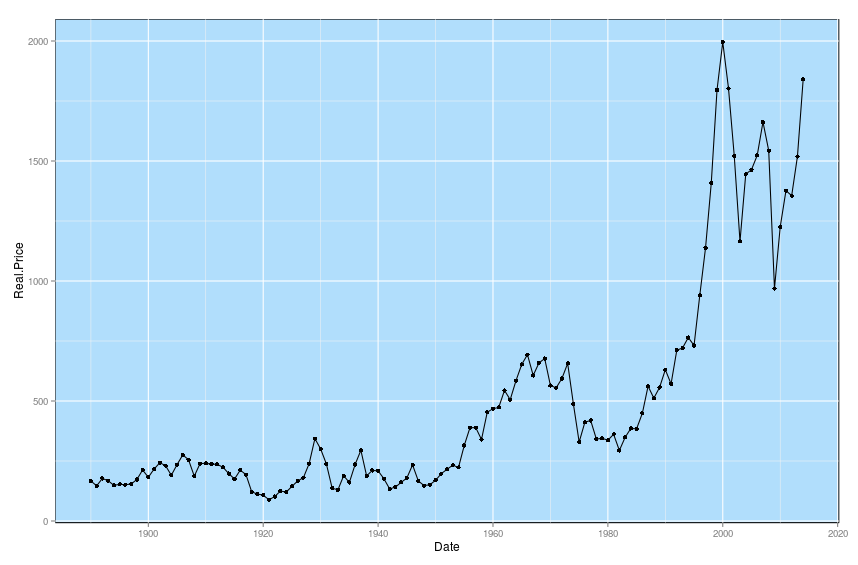

Inflation Adjusted Returns on Stocks

This chart shows the inflation adjusted returns on stocks going back to 1890. Notice the Y-values compared to housing. Clearly the value of stocks in aggregate rises much faster than a home that does not produce income.

×

Should you buy a house?

Sunday 05/11/14

A recent Gallup poll asked Americans what the best long-term investment was: bonds, real estate, stocks/mutual funds, gold, or savings accounts/CDs. The results showed that 30% of Americans believed that real estate was the best long term investment higher than any of the other choices. Are Americans right? Is real estate the best long-term investment? This week I want to discuss the pros and cons of real estate as an investment.Real Return

Real estate prices tend to keep up with inflation and not much more. The chart on the right shows the real house price going back to 1890. There is no indication that house prices will rise faster than the rate of inflation in the long-term. In fact, real estate tends to underperform stocks and bonds by a significant amount in the long run. The chart on the right shows the inflation adjusted returns of stocks over the same time period (notice the difference in magnitude of the y-values). So does this mean that real estate is a terrible investment that you should avoid? The answer is more complicated.

If your investment plan is to buy real estate and just leave it empty, then yes, real estate is definitely a bad investment. However, most people either plan to live in their property or rent it out. A real estate investment trust or REIT is a company that owns real estate that produces income and can be publicly traded similar to stocks. The Dow Jones Equity REIT index tracks the performance of equity REITs and has a total annualized return of 11.05% since inception December 31, 1989. This is very similar to the return of the S&P 500 over the same time period (the S&P 500 had an annualized return of 9.46% from 1990-2013, the long term average is lower).

Owning a home for personal use also has a number of intangible benefits like a sense of community, more control over design, etc. However, there are also costs that go into maintaining a home that you wouldn't pay if you were renting, such as repairs, taxes and interest payments. Proponents of housing sometimes assume that their full monthly payment is going into equity, but in reality, for most new homeowners, it is going into interest payments. If you were to take out a 30 year mortgage for $200,000 at a 4.25% interest rate, you will pay more in interest than towards home equity until February of 2028. Of course, when you are renting, none of your money is going into equity. A mortgage also adds a lot of leverage. For the average American homeowner, their home is the biggest leveraged investment that they will make. For an extreme example, consider an FHA loan where the minimum down payment is only 3.5%. For a $200,000 home, this means a down payment of $7,000 and a mortgage of $193,000. Imagine if I were to pitch the idea that you should take out a $193,000 loan to buy one stock, you'd think I was crazy, also no banker in their right mind would give you that loan. The average American homeowner is making a wildly speculative bet on their home and doesn't even realize it. This leverage means that all gains and losses are amplified, most homeowners really underestimate this risk.

There are also major tax benefits to owning a home, such as the ability to deduct mortgage interest and in many cases the exclusion of capital gains taxes when selling your primary residence. There are also many other miscellaneous tax credits and deductions related to housing on both the state and federal levels.

Conclusion

So is owning better than renting? The answer is that it depends on your personal preference. If you sold your home in 2006 and rented out a condo, you probably aren't regretting that decision. Likewise if you bought your first home in 2009 you are probably pretty happy about your purchase. Housing, like any other investment has its ups and downs and there is no right answer. Skill and luck can play a huge role in your success as a real estate investor and everyone would do well to think deeply about the risks they are taking when getting a mortgage.

| Index | Closing Price | Last Week | YTD |

|---|---|---|---|

| SPY (S&P 500 ETF) | 187.96 | 0.44% | 1.77% |

| IWM (Russell 2000 ETF) | 110.03 | -0.98% | -4.62% |

| QQQ (Nasdaq 100 ETF) | 86.8 | -0.21% | -1.32% |

Case Shiller Home Price Index

Inflation Adjusted Returns on Stocks