PowerShares UUP - DB US Dollar Index Bullish Fund

UUP is a fund that seeks to track changes, in the level of the Deutsche Bank Long US Dollar Index Futures Index. More information at <a href=https://www.invesco.com/portal/site/us/financial-professional/etfs/product-detail?productId=uup>Invesco</a>.

×

Euro/USD

This chart shows the value of one Euro per US doller. The higher the number the more valuable the Euro and vice versa. I have noted the approximate times of ECB rate changes.

×

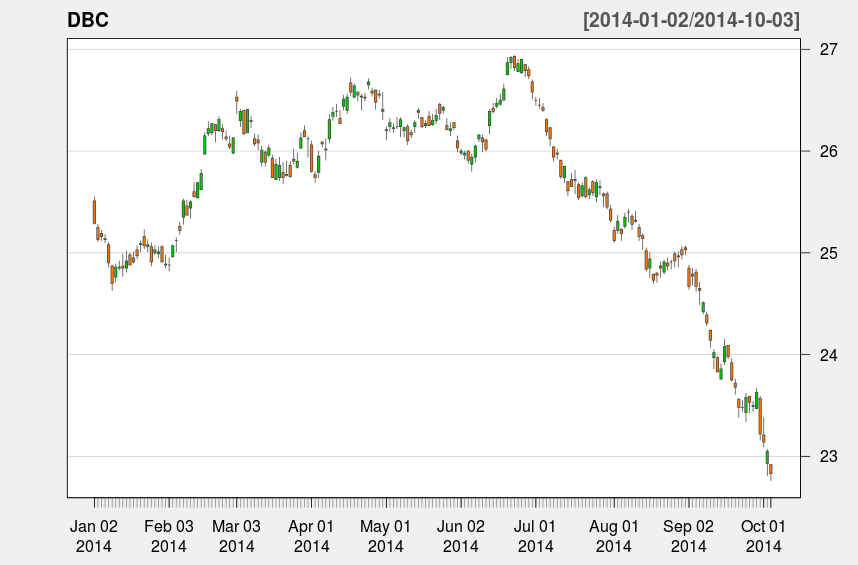

DBC - PowerShares DB Commodity Index Tracking Fund

The PowerShares DB Commodity Index Tracking Fund seeks to track changes, whether positive or negative, in the level of the DBIQ Optimum Yield Diversified Commodity Index. Visit Invesco for more information.

×

King Dollar

Sunday 10/05/14

Last week the markets dipped, but recovered most of their losses in a big end of the week rally. To me the most interesting change in the markets has been the strength of the U.S. dollar. The U.S. dollar has appreciated quite a bit in just the last few months as you can see from the first chart on the right. Any large move like this in the world's reserve currency will have major global effects. This week I want to look at some of the possible causes for the dollar's strength as well as potential consequences.

Possible Causes

I say 'possible causes' because the reasons for dollar strength are numerous and impossible to fully determine. Nevertheless, I will try to provide some of what I believe to be the biggest driving factors. Keep in mind that there is no single measurement for the dollar. The dollar can be measured in euros, yen, pounds, gold, oil, corn, coffee, underwear, you name it. Let's start by looking at the value of the euro in terms of dollars.

I believe the biggest reason for the recent strength in the US dollar is driven by the European Central Bank (ECB). In an attempt to fend off what increasingly looks like a triple-dip recession in Europe, the ECB lowered the deposit rate first to -0.10% on June 5th and then unexpectedly lowered it again to -0.20% on September 4th. As you can see from the chart on the right, the value of the euro relative to the dollar has fallen substantially since then. The ECB is hoping that instead of parking money at the ECB, that European banks will lend it out or invest it. However, it seems like they may be moving their money to the U.S. instead where they can get a safe yield at the Fed. This could lead to stress for European money markets, but that is a different newsletter.

Growth is slowing around the world, but the U.S. economy is still grinding along even if it is at a very slow pace. The growth rate in China is still very high, but there are signs that it may be coming to an end. This has manifested itself in commodities partly because China is the world's largest consumer of commodities. China used more cement from 2011-2013 than the United States used in the entire 20th century. China has experienced a massive housing bubble and over-development along with a huge expansion of debt in its shadow banking system. Now that credit is slowing, growth is slowing again in China. Recent economic datapoints suggest that this slowdown is far from over.

China isn't the only reason that commodities have been weak. This year was a record year for crops, especially corn, which is the cornerstone of American agriculture. As a result, prices have collapsed in corn, wheat, soybeans and other agricultural commodities. Oil and natural gas prices have moved steadily lower in the United States. There are a number of factors contributing to falling energy prices, but the main reason is technological breakthroughs in hydraulic fracturing and horizontal drilling, which I have discussed previously here. The U.S. is now the largest producer of oil and natural gas in the world overtaking both Russia and Saudi Arabia. As U.S. companies export this technology to other countries it should keep longterm downward pressure on oil prices.

I should also mention that this is the last month for quantitative easing in the United States. The Fed has also hinted that it may raise interest rates in the second half of 2015. If messaging becomes more clear, this could lead to an even stronger rally in the U.S. dollar.

Lastly, U.S. and E.U. sanctions on Russia have been leading to capital flight. Much of that money is likely coming back to the United States which is helping the dollar. Russia's currency is also collapsing as a result.

Consequences?

The consequences depend on who you are. If you are a saver in the U.S., this is a good thing, because your dollars can now buy more corn, gas prices are coming down, and you can take a cheaper vacation to Europe. However, if you have a lot of debt, then a rising dollar negatively impacts you, because you are paying back loans with more valuable dollars. If you are a lender, then a strong dollar is a good thing, because you are getting back more valuable dollars. This is a major problem for emerging market companies that took out loans denominated in U.S. dollars and are now trying to repay those loans with their weaker currencies. On the other hand, if you are a lender then you should be happy to receive those more valuable dollars. Large U.S. companies doing business overseas will also be negatively impacted as they convert their overseas currencies back into U.S. dollars.

Conclusion

A strong dollar can be concerning because it often precedes market panics. As investors become more anxious the value of the dollar rises. As mentioned earlier, since it is bad for multinationals doing business overseas, earnings could be weaker from large cap companies in the coming quarters. I would prefer to invest in U.S. businesses that get most of their sales from within the U.S.

| Index | Closing Price | Last Week | YTD |

|---|---|---|---|

| SPY (S&P 500 ETF) | 196.52 | 0.16% | 6.41% |

| IWM (Russell 2000 ETF) | 109.65 | -0.15% | -4.95% |

| QQQ (Nasdaq 100 ETF) | 98.17 | 0.38% | 11.61% |

PowerShares UUP - DB US Dollar Index Bullish Fund

Euro/USD

DBC - PowerShares DB Commodity Index Tracking Fund